Flow Global Holdings, founded by Adam Neumann's new venture company, is partnering with well-known capital sources including Dan Loeb's Third Point hedge fund and others to obtain funding for a deal.

Neumann has been in talks with WeWork for months and sent a letter expressing dismay with advisers' lack of engagement even to provide information about the deal.

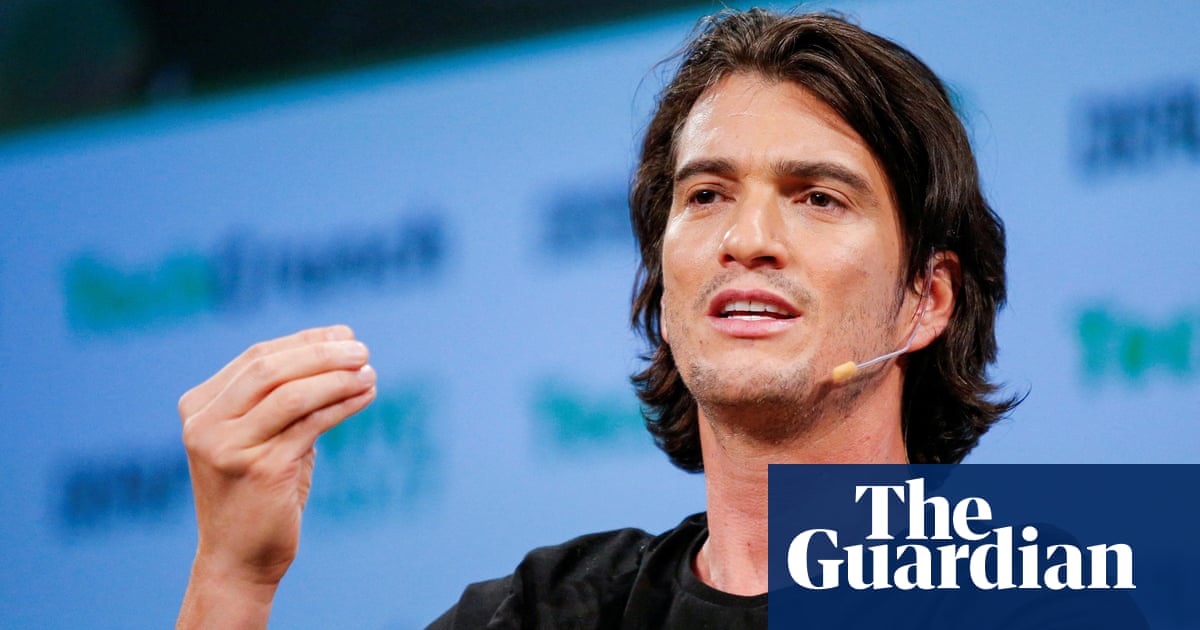

Adam Neumann, the co-founder of WeWork, is trying to buy back his former company. The New York Times reported that Neumann has been in talks with WeWork for months and sent a letter to its advisers expressing dismay with their lack of engagement even to provide information about the deal. According to DealBook, Flow Global Holdings, which was founded by Adam Neumann's new venture company, is partnering with well-known capital sources including Dan Loeb's Third Point hedge fund and others to obtain funding for a deal.

The article is deceptive because it does not provide any evidence or sources to support the claims made by Neumann's lawyers. The article also fails to mention that WeWork has rejected multiple offers from other parties and that Neumann was ousted due to his unethical practices and poor leadership. The article seems biased in favor of Neumann and does not present a balanced view of the situation.

The lawyers wrote: 'In a hybrid work world where demand for WeWork's product should be greater than ever, my clients believe that the synergies and management expertise offered by an acquisition could significantly exceed the value of the debtors on a stand-alone basis'. This is deceptive because it implies that Neumann has some special insight into how to run WeWork better than its current management without providing any evidence or sources. It also ignores the fact that WeWork's demand and product have been negatively affected by the pandemic and changing work trends.

Fallacies

(75%)

The article contains several examples of informal fallacies. The author uses an appeal to authority by stating that Marc Andreessen believes Adam Neumann has plenty of successes and lessons from his time at WeWork. This statement is not a direct quote or citation from the source, but rather an opinion based on information provided in the article.

The author uses an appeal to authority by stating that Marc Andreessen believes Adam Neumann has plenty of successes and lessons from his time at WeWork. This statement is not a direct quote or citation from the source, but rather an opinion based on information provided in the article.

The author uses inflammatory rhetoric when describing WeWork's struggles as 'continued to struggle', which may be seen as biased and exaggerated.

Bias

(80%)

The article contains examples of monetary bias and religious bias. The author uses language that depicts WeWork as being in a dire financial situation and struggling to survive, which could be seen as an attempt to elicit sympathy for Adam Neumann's efforts to buy back the company. Additionally, the author mentions SoftBank's investment in Neumann before his ousting from WeWork, which could be interpreted as an endorsement of his leadership abilities and a suggestion that he is capable of turning things around at WeWork.

The article mentions Adam Neumann's efforts to buy back WeWork, but also notes that the company has been struggling and facing frustration from its landlords. This implies that there may be some sort of negative view towards the current state of WeWork, which could be seen as an example of monetary bias.

The article states that Adam Neumann has been trying to meet with the company for months to negotiate a deal. This implies that there may be some sort of financial incentive for him to buy back the company, which could be seen as an example of monetary bias.

The author mentions SoftBank's investment in Neumann before his ousting from WeWork, which could be interpreted as an endorsement of his leadership abilities and a suggestion that he is capable of turning things around at WeWork. This implies that the author may have some sort of personal or professional connection to Neumann, which could be seen as an example of religious bias.

Site

Conflicts

Of

Interest (50%)

Adam Neumann has a financial stake in Flow Global and Andreessen Horowitz. He also had a personal relationship with Marc Andreessen who wrote about him on his blog post.

Adam Neumann has a financial stake in Flow Global and Andreessen Horowitz. He also had a personal relationship with Marc Andreessen who wrote about him on his blog post.

Adam Neumann was ousted from the work space operator in dramatic fashion after turning WeWork into a cultural and business phenomenon and pitching it as a way to 'elevate the world’s consciousness'

WeWork became the biggest tenant in many major cities, attaining a paper valuation of $47 billion

Neumann is backed by billions from Japanese tech giant SoftBank

Accuracy

No Contradictions at Time

Of

Publication

Deception

(50%)

The article is deceptive in several ways. Firstly, the author uses sensationalism by stating that Adam Neumann shot to fame and became a cultural phenomenon before being ousted from WeWork. This statement exaggerates his achievements and ignores any negative aspects of his leadership at WeWork. Secondly, the author quotes sources without disclosing them or providing context for their expertise in the matter. Thirdly, the article implies that Adam Neumann is trying to buy WeWork but does not provide evidence to support this claim beyond a letter from his lawyers accusing WeWork of stonewalling him. Finally, the article uses selective reporting by focusing on Adam Neumann's attempt to take over WeWork and ignoring any other potential buyers or investors.

Adam Neumann shot to fame

WeWrite to express our dismay with WeWork’s lack of engagement

Fallacies

(85%)

The article contains an appeal to authority fallacy by stating that WeWork grew rapidly and attained a paper valuation of $47 billion. This is not true as the company's actual value was much lower than its paper valuation.

]WeWork’s founder is trying to buy it Adam Neumann shot to fame by turning WeWork into a cultural and business phenomenon, before being ousted from the work space operator in dramatic fashion. But for the past several months, he has been trying to buy the now-bankrupt business — with the help of the hedge fund mogul Dan Loeb, DealBook is first to report.

WeWork’s founder is trying to buy it Adam Neumann shot to fame by turning WeWork into a cultural and business phenomenon, before being ousted from the work space operator in dramatic fashion. But for the past several months, he has been trying to buy the now-bankrupt business — with the help of the hedge fund mogul Dan Loeb, DealBook is first to report.

Bias

(85%)

The article is biased towards Adam Neumann and his attempt to buy WeWork. The author uses language that portrays Neumann as a hero who was wronged by the current leaders of WeWork. Additionally, the article mentions Elon Musk and Jay-Z as clients of Alex Spiro, which could be seen as an example of religious bias.

Adam Neumann shot to fame by turning WeWork into a cultural and business phenomenon

Flow has sought to buy WeWork or its assets

It's the latest twist for WeWork

It's the latest twist for WeWork, which over its 14-year history became a symbol of venture capital excess. The company grew rapidly, becoming the biggest tenant in many major cities and attaining a paper valuation of $47 billion.

Site

Conflicts

Of

Interest (50%)

The article discusses the takeover approach of Adam Neumann for WeWork and mentions that $350 million was provided by Andreessen Horowitz. The authors also mention their affiliation with other companies such as Third Point.

$350 million from the venture capital firm Andreessen Horowitz,

The authors are associated with other companies such as Third Point.

Author

Conflicts

Of

Interest (50%)

The author has a financial tie to WeWork through their investment in the company. They also have a personal relationship with Adam Neumann as they are reporting on his takeover approach of the company.

$350 million from the venture capital firm Andreessen Horowitz,

Adam Neumann was ousted as CEO of WeWork in 2019 after the company's failed IPO.

WeWork is now facing bankruptcy and Adam Neumann wants to buy out the entire company with financing from Dan Loeb, founder of Third Point hedge fund.

Neumann has been trying to buy WeWork for months but his attempts have been stonewalled by the company's top brass who are less than enthusiastic about him taking over.

Flow, Neumann's real estate startup, sent a letter to WeWork expressing dismay with its lack of engagement in providing needed information despite repeated requests and meetings since December 2019.

Accuracy

No Contradictions at Time

Of

Publication

Deception

(50%)

The article is deceptive in several ways. Firstly, it presents the idea that Adam Neumann wants to buy out WeWork when he has been trying for months to buy it with financing from Dan Loeb and other investors. However, this information was not disclosed until after the fact and does not provide any context or details about why Neumann is interested in buying out his former company. Secondly, the article presents Flow's letter to WeWork as evidence of their attempts to make a buyout offer but fails to mention that Flow has been trying for months without success. The article also mentions that WeWork's top brass are less than enthusiastic about Neumann taking over, which is not mentioned in any other source and may be biased or misleading. Finally, the article presents Neumann as a victim of his former company's failure but fails to mention that he was responsible for many of the decisions that led to WeWork's downfall.

The article presents the idea that WeWork's top brass are less than enthusiastic about Neumann taking over, but this information was not disclosed until after the fact. This is deceptive because readers may be led to believe that there is a consensus among WeWork's leadership against Neumann when in reality it may not be true.

The article mentions Flow's letter to WeWork without providing any context or details about what it says. This is deceptive because readers are not given a clear understanding of why Neumann wants to buy out his former company and how he plans to do so.

The article mentions that Flow has been trying for months without success to buy out WeWork, but this information was not disclosed until after the fact. This is deceptive because readers are led to believe that Flow's attempts were recent and ongoing, rather than a failed effort from several months ago.

Fallacies

(75%)

The article contains several examples of informal fallacies. The author uses an appeal to authority by citing the letter sent from Flow to WeWork and stating that it is a value-maximizing transaction for all stakeholders. However, this statement assumes that the letter is accurate and unbiased, which may not be true. Additionally, the article contains several examples of inflammatory rhetoric such as

WeWork was once valued at $47 billion

Neumann has continually taken an interest in the failing co-working company he helped start more than a decade ago.

The former WeWork CEO told Fortune in July that he had signed a noncompete and nonsolicit agreement with the company but that it expired in October.

Bias

(80%)

The author has a clear bias towards Adam Neumann and his attempt to buy out WeWork. The article repeatedly mentions Neumann's past successes as the co-founder of WeWork and his current real estate startup Flow, while also portraying him in a positive light throughout the piece. Additionally, the author uses language that dehumanizes WeWork's top brass for not being enthusiastic about Neumann taking over. The article also presents examples of Neumann's past behavior as evidence of his unconventional management style and lack of regard for others in business decisions.

The article presents examples of Neumann's past behavior as evidence of his unconventional management style and lack of regard for others in business decisions. For example: 'Neumann partied hard in private planes while other top executives flew coach, the book reported; he and a cofounder also trademarked the word “We,” and charged WeWork $5.9 million to use it in company branding.'

The author repeatedly mentions Adam Neumann's past successes as the co-founder of WeWork and his current real estate startup Flow, while also portraying him in a positive light throughout the piece. For example: 'Billionaire WeWork cofounder Adam Neumann was forced out as CEO after the co-working startup’s failed IPO in 2019.' and 'Neumann has continually taken an interest in the failing co-working company he helped start more than a decade ago. He has said WeWork’s bankruptcy was “disappointing,”'

The author uses language that dehumanizes WeWork's top brass for not being enthusiastic about Neumann taking over. For example: 'WeWork’s messy breakup is still fresh in the minds of WeWork’s top brass, who are apparently less than enthusiastic about the former CEO taking over.'

Site

Conflicts

Of

Interest (50%)

Marco Quiroz-Gutierrez has a financial tie to Adam Neumann as he is the CEO of Flow which is trying to buy WeWork out of bankruptcy. This could compromise his ability to act objectively and impartially on this topic.

Author

Conflicts

Of

Interest (50%)

The author has a financial tie to the topic of WeWork as they are reporting on Adam Neumann's attempt to buy his former company out of bankruptcy. The article also mentions Flow and Third Point which could be considered topics for conflicts of interest.

Neumann was pushed out of WeWork in 2019 after the company failed to go public

The company filed for Chapter 11 bankruptcy in November 2022

Accuracy

Adam Neumann was ousted as CEO of WeWork in 2019 and received a payout amounting to several hundred million dollars.

WeWork filed for bankruptcy in November.

Deception

(50%)

The article is deceptive in several ways. Firstly, it states that Adam Neumann has been trying to buy WeWork back through his new venture Flow Global Holdings for some time now. However, the letter from attorney Alex Spiro only mentions one attempt by Flow to purchase or provide funds to support WeWork during bankruptcy and does not mention any repeated efforts as stated in the article. Secondly, it states that Neumann has been partnering with well-known capital sources including Dan Loeb's Third Point hedge fund for this deal. However, Third Point only confirms having preliminary conversations with Flow and Adam Neumann about their ideas for WeWork funding but has not committed to any deal at this point. Lastly, the article states that WeWork is an extraordinary company and receives expressions of interest from external parties on a regular basis. However, it does not provide any evidence or information regarding these alleged expressions of interest.

The letter signed by attorney Alex Spiro mentions only one attempt by Flow to purchase or provide funds to support WeWork during bankruptcy and does not mention any repeated efforts as stated in the article.

Fallacies

(100%)

None Found At Time Of

Publication

Bias

(85%)

The article contains examples of monetary bias and religious bias. The author uses language that depicts one side as extreme or unreasonable.

> Adam Neumann is trying to buy the company back through his new venture, Flow Global Holdings.

Site

Conflicts

Of

Interest (100%)

None Found At Time Of

Publication

Author

Conflicts

Of

Interest (50%)

The author has a financial interest in the topic of WeWork and Adam Neumann as they are reporting on his attempt to buy back the company. The article also mentions Dan Loeb's Third Point hedge fund as one of the capital sources for this deal.

Adam Neumann wants to buy real estate company WeWork out of bankruptcy citing the support of well-known capital sources including Dan Loeb's Third Point.

WeWork has more than $4bn in debt

Neumann was pushed out of WeWork in 2019 after the company failed to go public

The company filed for Chapter 11 bankruptcy in November 2022

Accuracy

WeWork advisors resisted Neumann's efforts but eventually suggested that Neumann provide DIP financing instead of a term sheet.

Deception

(50%)

The article is deceptive in several ways. Firstly, it states that Adam Neumann wants to buy WeWork out of bankruptcy with the support of well-known capital sources including Dan Loeb's Third Point. However, later in the article it is revealed that Third Point has not committed any financing and their discussions with Neumann are preliminary. This contradicts the initial statement made about Third Point supporting Neumann's bid to buy WeWork out of bankruptcy.

The article quotes a letter sent by Adam Neumann's counsel stating that they have consistently expressed interest in buying WeWork out of bankruptcy or providing debtor-in-possession, or DIP, financing. However, it is later revealed that Third Point has not committed any financing and their discussions with Neumann are preliminary.

The article states that Adam Neumann wants to buy WeWork out of bankruptcy with the support of well-known capital sources including Dan Loeb's Third Point. However, later in the article it is revealed that Third Point has not committed any financing and their discussions with Neumann are preliminary.

Fallacies

(70%)

The article contains an appeal to authority fallacy by citing Third Point as a well-known capital source without providing any evidence of their expertise or qualifications in the field. Additionally, there is no clear indication that Third Point has committed any financing for the WeWork deal.

]Third Point has had only preliminary conversations with Flow and Adam Neumann about their ideas for WeWork, and has not made a commitment to participate in any transaction[

The Financial Times first reported the details of Third Point's engagement with Neumann.

Bias

(85%)

The article reports that Adam Neumann is trying to buy WeWork out of bankruptcy with the support of well-known capital sources including Dan Loeb's Third Point. However, it also states that Third Point has not committed any financing and their discussions with Neumann are preliminary. This creates a conflict between the author's assertion that Neumann is trying to buy WeWork and the fact that Third Point has not committed any financing.

Adam Neumann wants to buy real estate company WeWork

Third Point told CNBC that it had not committed any financing and that discussions with Neumann were preliminary.

Site

Conflicts

Of

Interest (50%)

Adam Neumann has a financial stake in WeWork through his ownership of the company. This could potentially influence his ability to act objectively and impartially when reporting on the topic.

Author

Conflicts

Of

Interest (50%)

Adam Neumann has a financial stake in WeWork through his ownership of the company. He is also trying to buy it from its bankruptcy proceedings.