Global corporate bond spreads have widened for the first time in a year.

Spreads on both junk and investment-grade notes have widened by approximately 10 basis points in June.

Yield premiums on corporate bonds are also rising from May levels, observed for less than 1% of the period since the 2008 global financial crisis.

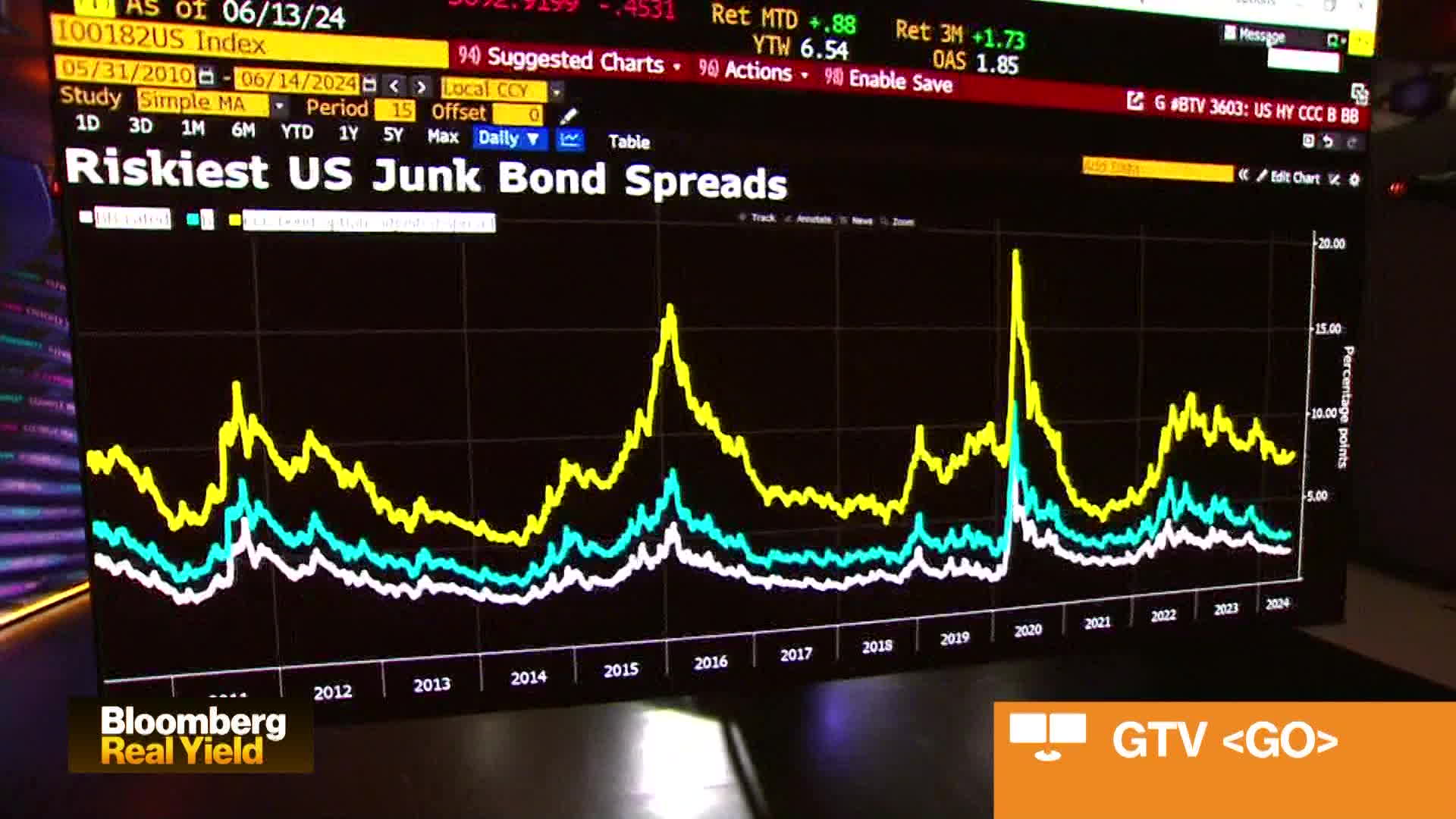

Global corporate bond spreads, a key indicator of credit market health, have experienced their first month of weakening since late last year. This development has rekindled the debate about the value of credit versus other fixed-income classes as investors navigate the second half of 2024. According to data from Bloomberg, spreads on corporate bonds including junk and investment-grade notes have widened by approximately 10 basis points in June. This marks a departure from their lowest levels seen in three years.

Moreover, yield premiums on these bonds are also rising from May 2024 levels which have only been observed for less than 1% of the period since the 2008 global financial crisis. These trends suggest that investors may be re-evaluating their risk tolerance in light of potential economic uncertainties.

Despite these developments, it is essential to consider various perspectives when assessing the credit market landscape. For instance, Citigroup's Head of U.S. Credit Strategy Michael Anderson raises the question:

Global corporate bond spreads have widened by about 10 basis points in June 2024.

Spreads on corporate bonds, including junk and investment-grade notes, are at their lowest levels in three years.

Yield premiums on corporate and US high-grade bonds are rising from May 2024 levels seen only for less than 1% of the period since the 2008 global financial crisis.

Accuracy

Spreads on corporate bonds including junk and investment-grade notes have widened by about 10 basis points so far in June.

US high-grade spreads are forecasted to end 2024 at 90 basis points and junk spreads at 291, compared with current Bloomberg index levels of 94 basis points and 314 basis points, respectively.

Michael Best, Portfolio Manager at Barings, and Andrea DiCenso, Co-Portfolio Manager at Loomis, discussed high yield and stresses on Bloomberg Real Yield.

Global corporate bond spreads are on track to turn in their first month of weakening since late last year, reigniting the debate about the relative value of credit versus other fixed-income classes heading into the second half of 2024.

US high-yield debt issuers have shown broad-based deterioration in the first quarter with profit margins dropping to a three-year low, though leverage was comfortably below the long-term average.

Accuracy

Global corporate bond spreads are on track to turn in their first month of weakening since late last year

US high-grade spreads are forecasted to end 2024 at 90 basis points and junk spreads at 291, compared with current Bloomberg index levels of 94 basis points and 314 basis points, respectively.

European junk bonds may deliver 5% in excess returns in 2024, while their US equivalents may generate 3.7%

US dollar-denominated corporate bonds have tighter valuations than Australian credits

Deception

(100%)

None Found At Time Of

Publication

Fallacies

(95%)

The article contains some instances of appeals to authority and inflammatory rhetoric, but overall the authors provide a clear and objective analysis of the current state of corporate bond markets. They quote experts in the field to support their arguments and do not make any fallacious claims or assumptions. The authors also provide specific data points to back up their assertions, such as spread levels and yield premiums.

][Neeraj Seth]’s chief investment officer and head of Asia-Pacific fundamental fixed income at BlackRock Inc. in Singapore” says “That’s normally a “good environment” for credit,