In recent months, the housing market has become a significant challenge for consumers due to rising home prices and inflation. According to various reports, homebuyers are feeling more distressed as they struggle to afford properties in the current market conditions. The Federal Reserve's tightening campaign to curb inflation and a chronic lack of supply have contributed to this housing affordability crisis.

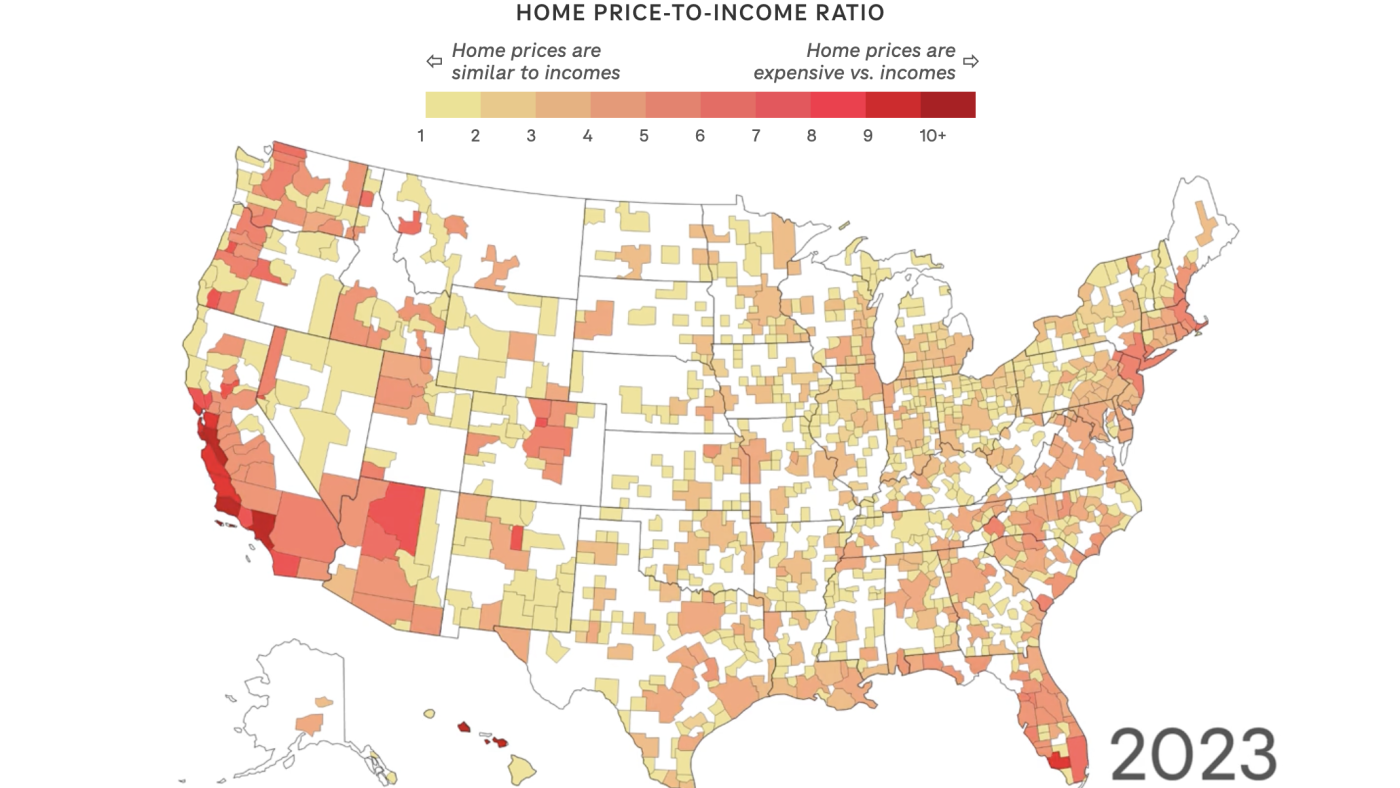

As per data from the Harvard Joint Center for Housing Studies, U.S. home prices have increased by 47% since early 2020. In nearly half of metro areas, buyers must make more than $100,000 to afford a median-priced home (NPR). Rising property taxes and insurance rates are adding to the financial strain for both homeowners and renters.

Stella Bermema from Tampa Bay feels suffocated by these rising costs. She expressed her concerns on Fox News, stating that there are not enough listings available due to mortgage rates remaining low in 2019 (Fox Business). Anthony Fumo's family is also considering renting due to the current housing market conditions and lack of space in their current home.

Lennar, a homebuilder, reported that consumers are under increasing pressure from price increases and looking for incentives or discounts to afford homes (Yahoo Finance). The Federal Reserve anticipates one interest rate cut this year, which could potentially activate pent-up demand if it leads to lower mortgage rates.

Danielle Hale, Chief Economist at Realtor.com, warned that the housing market may hit a 'breaking point' as high borrowing costs for home loans and rising home prices have made homebuying out of reach for a large portion of Americans (Newsweek). Price increases have outpaced income growth, limiting potential buyers' ability to dedicate enough earnings towards purchasing a property.

It is essential to note that these reports come from various sources with different biases. While some sources may lean more towards the left, others may be right-leaning. It is crucial for readers to remain skeptical and consider multiple perspectives when evaluating housing market news.