Mortgage rates have risen for the second week, reaching 6.77%.

The average mortgage rate is based on mortgage applications that Freddie Mac receives from thousands of lenders across the country.

Mortgage rates have risen for the second week, reaching 6.77%. The average mortgage rate is based on mortgage applications that Freddie Mac receives from thousands of lenders across the country. Inflation remains stubbornly high and is contributing to rising mortgage rates. Strong employment data has also contributed to rising interest rates.

The average mortgage rate is based on mortgage applications that Freddie Mac receives from thousands of lenders across the country.

Inflation remains stubbornly high and is contributing to rising mortgage rates.

Strong employment data has also contributed to rising interest rates.

Accuracy

Mortgage rates rose for the second week, reaching 6.77%

Deception

(50%)

The article is deceptive in that it presents the idea that mortgage rates are rising due to strong employment and inflation reports. However, this is not entirely accurate as there are other factors at play such as supply and demand for homes. The author also uses quotes from experts without providing any context or explanation of their opinions.

Mortgage rates increased this week due to consumer prices rising more than expected

The 30-year fixed-rate mortgage averaged 6.77% in the week ending February 15, up from 6.64% the previous week

Fallacies

(85%)

The article contains several fallacies. The author uses an appeal to authority by citing the opinions of experts such as Sam Khater and Bob Broeksmit without providing any evidence or context for their claims. Additionally, the author makes a false dichotomy by stating that mortgage rates are either increasing due to inflation or decreasing due to lower demand, when in reality there may be other factors at play. The article also contains inflammatory rhetoric by describing the housing market as being

The 30-year fixed-rate mortgage averaged 6.77% in the week ending February 15, up from 6.64% the previous week.

<strong>On</strong> <em><u>the heels of consumer prices rising more than expected, mortgage rates increased this week,

Bias

(85%)

The article reports that US mortgage rates jumped higher after a string of strong employment and inflation reports. The author quotes experts who attribute the rise in mortgage rates to these factors. Additionally, the article mentions that consumer prices rose more than expected which also contributed to the increase in mortgage rates.

Inflation remains stubbornly high Mortgage rates are climbing because the economy is still hot. In addition to strong employment numbers, the Consumer Price Index data for January, released on Tuesday, showed that inflation slowed less than expected last month.

]The economy has been performing well so far this year and rates may stay higher for longer, potentially slowing the spring homebuying season[

Mortgage rates have surged higher again, causing homebuyers to pull back.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 6.87% last week from 6.80% the week before, with points rising to 0.65 from 0.59 (including the origination fee) for loans with a 20% down payment.

Applications to refinance a home loan fell by two percent for the week but were twelve percent higher than the same week one year ago.

Accuracy

No Contradictions at Time

Of

Publication

Deception

(30%)

The article is deceptive in several ways. Firstly, the author claims that mortgage rates have surged higher again and this has caused homebuyers to pull back. However, they do not provide any evidence or data to support this claim. Secondly, the author quotes an MBA economist who states that purchase applications remained subdued as elevated rates continue to add to affordability challenges along with still-low existing housing inventory. This statement is misleading because it implies that all homebuyers are struggling with high mortgage rates and low housing inventory when in fact, the vast majority of current borrowers have loans with rates far lower than those available today.

The MBA economist states that purchase applications remained subdued as elevated rates continue to add to affordability challenges along with still-low existing housing inventory, which is misleading because it implies all homebuyers are struggling when in fact the vast majority of current borrowers have loans with lower rates.

The author claims that mortgage rates have surged higher again but does not provide any evidence or data to support this claim.

Fallacies

(70%)

The article contains several fallacies. The author uses an appeal to authority by citing the Mortgage Bankers Association and Redfin as sources for information about mortgage rates and homebuyer behavior. However, these organizations have a vested interest in promoting their own products or services, which may influence their reporting. Additionally, the article contains inflammatory rhetoric when it describes rising mortgage rates as

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 6.87% last week from 6.80% the week before, with points rising to 0.65 from 0.59 (including the origination fee) for loans with a 20% down payment.

The vast majority of current borrowers have loans with rates far lower than those available today.

Bias

(85%)

The article contains multiple examples of bias. The author uses language that dehumanizes and demonizes white supremacists who are celebrating the reference to a racist conspiracy theory in an online post. This is an example of religious bias as it implies that only one religion has extremist followers.

After a brief reprieve in December and January, mortgage rates are moving higher again,

Rooftops of homes in a gated residential community are seen in Pico Rivera, California on January 18, 2024. Frederic J. Brown | AFP | Getty Images

Site

Conflicts

Of

Interest (50%)

The author has a conflict of interest with the Mortgage Bankers Association as they are mentioned in the article and may have an affiliation or financial stake in them.

The average mortgage rate is based on mortgage applications that Freddie Mac receives from thousands of lenders across the country.

Inflation remains stubbornly high and is contributing to rising mortgage rates.

Strong employment data has also contributed to rising interest rates.

Accuracy

Mortgage rates rose for the second week, reaching 6.77%

Deception

(50%)

The article is deceptive in several ways. Firstly, the title of the article suggests that mortgage applications are declining due to rate changes and Federal Reserve speakers reacting to inflation reports. However, this information is not mentioned anywhere in the body of the article. Secondly, there are multiple instances where quotes from experts or studies are used without providing any context or disclosing their sources. This makes it difficult for readers to verify the accuracy of these statements. Thirdly, some sentences contain sensationalist language that could be misleading if taken out of context.

The title suggests that mortgage applications are declining due to rate changes and Federal Reserve speakers reacting to inflation reports. However, this information is not mentioned anywhere in the body of the article.

Fallacies

(85%)

The article discusses the potential impact of rate changes on mortgage applications and Federal Reserve speakers' reactions to inflation reports. The author also mentions buy now, pay later plans and their popularity among financially fragile shoppers. Additionally, the article touches upon inflation data and its importance in determining interest rates.

Mortgage loan application volume decreased by 2.3% for the week ending Feb 9,

Bias

(85%)

The article discusses the potential sensitivity of mortgage buyers to rate changes and Federal Reserve speakers' reactions to inflation reports. The Fed should proceed carefully on rate cuts due to limited historical experience with growth and inflation dynamics during a global pandemic. Buy now, pay later (BNPL) repayment plans are growing in popularity among financially fragile shoppers who use the product more often than stable consumers. Officials at the Federal Reserve have repeatedly said they want to gain confidence that inflation is on a downward trajectory before cutting their benchmark interest rate. Financial markets have continually pushed back their bets for when the Fed will cut its key interest rate from its current 23-year high where it has been held since July to quash inflation.

The Federal Reserve should proceed carefully on rate cuts due to limited historical experience with growth and inflation dynamics during a global pandemic.

Site

Conflicts

Of

Interest (50%)

The article discusses the topic of mortgages and rate changes. The author is Michael Barr who has a financial stake in banks that offer buy now pay later plans (BNPL). Additionally, the Federal Reserve speakers mentioned are Austan Goolsbee and Felix Aidala who have previously spoken about BNPL products.

Austan Goolsbee is mentioned as a previous speaker on the topic of BNPL products.

Michael Barr discusses his role as former Vice Chairman of the Federal Reserve Board and how he has been involved in discussions around buy now pay later plans (BNPL).

Home prices posted their biggest annual increase in 15 months

Mortgage rates rose this week to an average of above 7%

High housing costs and seasonal factors like extreme storms in Southern California pushed down pending sales by 7.3% year over year

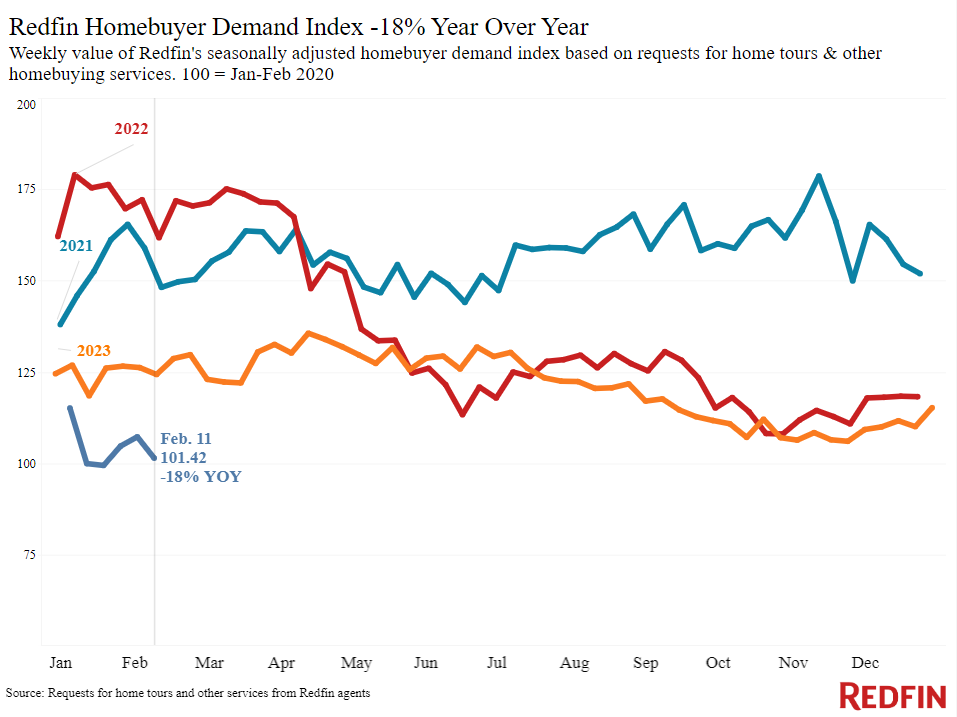

Redfin's Homebuyer Demand Index is down 18%, indicating a decrease in requests for tours and other homebuying services from Redfin agents

Accuracy

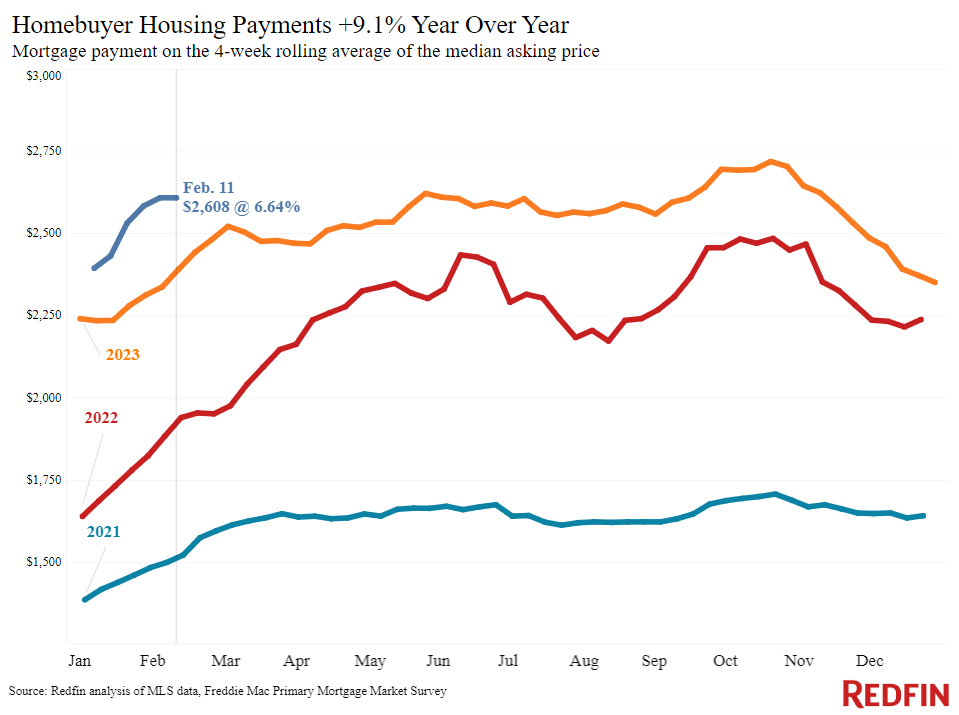

Home prices posted their biggest annual increase in 15 months, rising 6.1% year over year during the four weeks ending February 11

Mortgage rates rose this week to an average of above 7%, up from 6.6% at the beginning of the month

Deception

(30%)

The article is deceptive in several ways. Firstly, the author states that pending sales are down 7.3% year over year and Redfin's Homebuyer Demand Index is down 18%. However, they do not provide any context or explanation for these declines. It could be due to a variety of factors such as high housing costs or other economic conditions, but without further information it is difficult to determine the exact cause. Additionally, the author quotes several experts who make statements that are misleading or inaccurate. For example, Redfin Economic Research Lead Chen Zhao states that 'The Super Bowl is like Groundhog Day for real estate economists; we usually have a read on how the market is shaping up by the beginning of February'. However, this statement implies that the Super Bowl has a significant impact on the housing market which may not be entirely accurate. Finally, there are several instances where information presented in one part of the article contradicts information presented elsewhere. For example, while Redfin's Homebuyer Demand Index is down 18%, Google searches for 'home for sale' are essentially unchanged from a month earlier (as of Feb. 10). This suggests that there may be other factors at play which the author does not address.

The article states that pending sales are down 7.3% year over year and Redfin's Homebuyer Demand Index is down 18%. However, it does not provide any context or explanation for these declines.

Fallacies

(100%)

None Found At Time Of

Publication

Bias

(100%)

None Found At Time Of

Publication

Site

Conflicts

Of

Interest (50%)

Dana Anderson has conflicts of interest on the topics of home prices and mortgage rates as she is an employee of Redfin which operates in the housing market.

Author

Conflicts

Of

Interest (50%)

The author has a conflict of interest on the topic of home prices and mortgage rates as they are affiliated with Redfin which is mentioned in the article.

The Consumer Price Index (CPI) report for January showed a month-over-month increase in core inflation of 0.4%, higher than the expected 0.3% and previous month's 0.3%. This change suggests that the momentum of inflation is rising back toward levels from early 2023, after appearing to cool since September.

Mortgage rates rose for the second week, reaching 6.77%

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 6.87% last week from 6.80% the week before, with points rising to 0.65 from 0.59 (including the origination fee) for loans with a 20% down payment.

Applications for mortgage to purchase home dropped by three percent and were twelve percent lower than the same week a year ago.

Accuracy

Mortgage rates rose for the second week, reaching 6.77%, based on mortgage applications received by Freddie Mac from thousands of lenders across the country.

Deception

(80%)

The article is deceptive in several ways. Firstly, the author claims that inflation is the biggest reason for mortgage rates moving higher at a pace seen in 2022/2023. However, this statement contradicts other information provided in the article which states that CPI was not responsible for rising interest rates but rather it was due to supply chain disruptions and global economic factors. Secondly, the author claims that today's CPI data is highly consequential as it confirms what many had suspected about inflation momentum cooling down since last September. However, this statement is also false as the report shows a rise in inflation back towards early 2023 levels which contradicts previous statements made by the author. Lastly, the article uses sensationalist language such as

Small monthly changes are very important when it comes to CPI--especially if those changes make a new argument about the momentum of inflation.

The bond/rate market was essentially asking itself if it had been caught flat-footed heading into February.

Fallacies

(85%)

The article contains several fallacies. The first is an appeal to authority when the author states that inflation is the biggest reason rates moved higher at the pace seen in 2022/2023 without providing any evidence or data to support this claim.

Bias

(85%)

The author demonstrates bias by implying that the Consumer Price Index (CPI) is the biggest market mover among inflation reports and therefore should be given more focus. This is an example of monetary bias as it suggests that CPI has a greater impact on markets than other inflation indicators.

If it feels like there’s been an inordinate amount of focus on the Consumer Price Index (CPI) recently, today proved it was justified.

Site

Conflicts

Of

Interest (50%)

Matthew Graham has a conflict of interest on the topic of Mortgage Rates as he is an owner and publisher of Mortgage News Daily. He also has a financial stake in the bond market which could influence his coverage.

Author

Conflicts

Of

Interest (50%)

The author has a conflict of interest on the topic of Mortgage Rates as they are reporting on it. The article mentions that mortgage rates have been affected by inflation and this could be seen as an attempt to influence public opinion or sway consumer behavior.

:max_bytes(150000):strip_icc()/GettyImages-1468619438-f87f0a88bab342fe8244c6e40871db0d.jpg)