Consumer-driven economy supporting growth in rest of world.

Elections in various countries could result in significant shifts in political leadership and investment environments globally.

India generating strong manufacturing capacity due to expected 6.8% growth rate this year.

Inflation has retreated sharply in major developed economies and central banks are implementing monetary policy outlooks including higher-for-longer interest rates and borrowing costs.

The US, as the world's largest economy, is driving global growth with a predicted expansion rate more than twice that of other major developed countries.

US economy has better momentum than other major economies with real GDP growth estimates seeing upward revisions, household spending remaining resilient, and labor market churning out new jobs at a solid pace with higher wages.

The United States, as the world's largest economy, is playing a crucial role in global growth amidst weak economic activity in Europe and China. The International Monetary Fund predicts that the US economy will expand this year at more than twice the rate of other major developed countries. This consumer-driven economy is supporting growth in the rest of the world as well. The U.S., India, and Japan are generating strong tailwinds for global economic growth (Capital Group economists). Despite higher interest rates and elevated inflation, many companies are looking to India as an additional source of manufacturing capacity due to its expected 6.8% growth rate this year (IMF projections). However, elections in various countries, including the U.S., could result in significant shifts in political leadership and investment environments globally.

The economic outlook is contradictory with global markets being ebullient while institutions issue warnings about economic fragmentation. The idea of an interdependent global economy functioning within a geopolitical system based on national sovereignty has always reflected a certain amount of idealism or hubris. This marriage did collapse in the 1930s and lasted through the end of World War II (Japantimes).

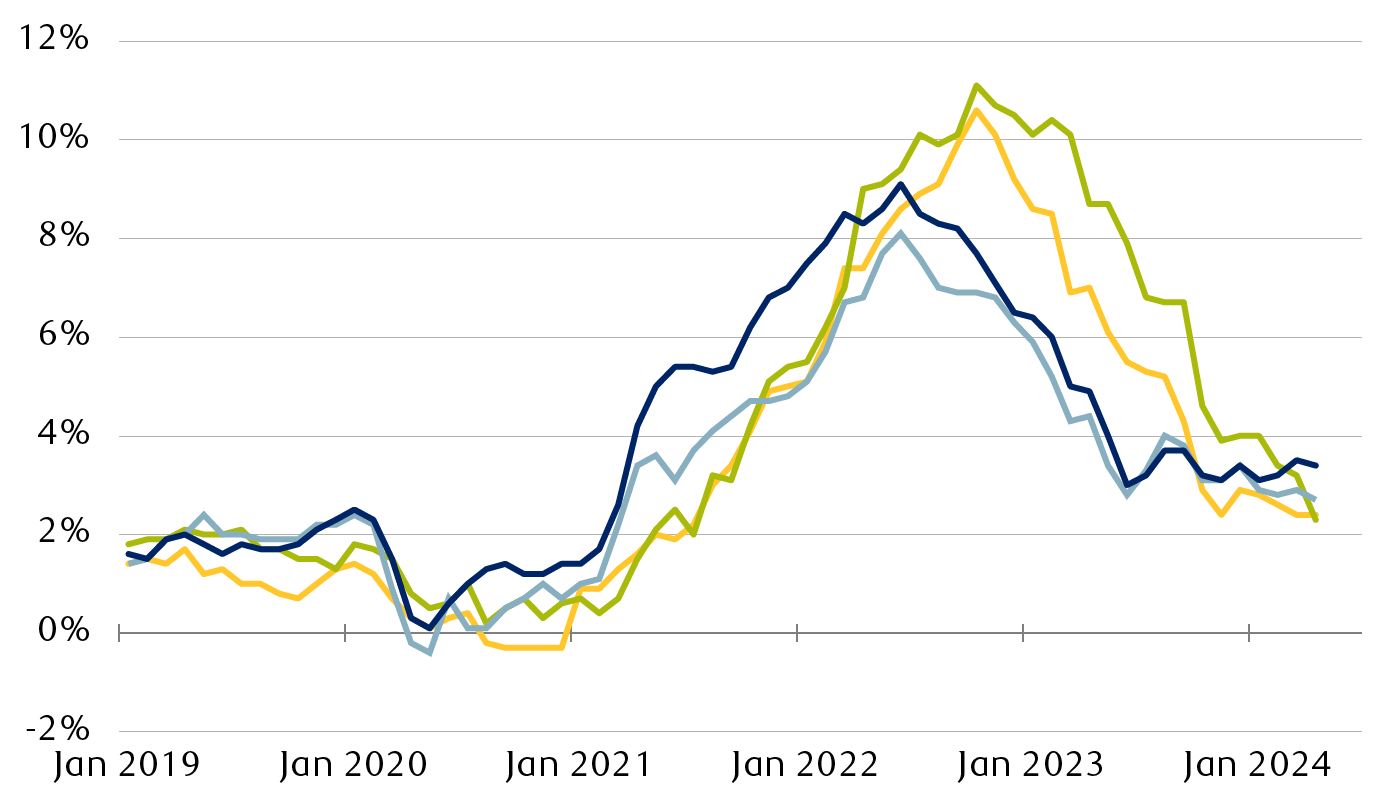

The U.S. economy has better momentum than other major countries, with real GDP growth estimates seeing significant upward revisions for the U.S., household spending remaining resilient, and labor market churning out new jobs at a solid pace with higher wages (RBC Wealth Management). Inflation has retreated sharply in major developed economies, and headline consumer inflation year over year is between 2% and 4% for all regions shown. Central banks are implementing monetary policy outlooks, including higher-for-longer interest rates and borrowing costs (RBC Wealth Management).

The European Central Bank cut its benchmark rate by 0.25%, but inflation data has consistently come in hotter than expected, and the US economy's strength has defied expectations (Business Insider).

The European Central Bank cut its benchmark rate by 0.25% on Thursday.

Inflation data has consistently come in hotter than expected and the US economy’s strength has defied expectations.

Accuracy

]The European Central Bank cut its benchmark rate by 0.25% on Thursday.[

Investors and economists expect the Federal Reserve to follow suit and cut interest rates in September.

Central banks around the world are coordinating their descent into a soft landing.

Deception

(30%)

The article contains several instances of sensationalism and selective reporting. The author states that 'everything must go right, or global markets could turn violent' and 'reality has been making a mockery of experts’ assumptions all year long'. These statements are sensational in nature as they create a sense of urgency and fear without providing any concrete evidence to support the claims. Additionally, the author selectively reports on inflation data and economic growth expectations, implying that these are the only factors at play when making predictions about interest rate cuts. However, there are other factors such as geopolitical tensions and global supply chain disruptions that could also impact central banks' decisions.

Reality has been making a mockery of experts’ assumptions all year long.

Everything must go right, or global markets could turn violent.

Fallacies

(85%)

The author uses an appeal to authority fallacy when stating 'Experts have assumed all year long that inflation would cool off, the economy would slow to a more leisurely pace of growth, and as many as six interest rate cuts from the Fed.' This statement implies that the assumptions made by experts are factual and infallible, which is not true. Additionally, there are instances of inflammatory rhetoric such as 'Wall Street thinks we’re in for stagflation; the next, it believes a soft landing is coming' and 'This divergence has the potential to bring that same frantic energy to currency markets.' These statements create an emotional response without providing any concrete evidence or reasoning.

]Experts have assumed all year long that inflation would cool off, the economy would slow to a more leisurely pace of growth, and as many as six interest rate cuts from the Fed.[

Wall Street thinks we’re in for stagflation; the next, it believes a soft landing is coming.

This divergence has the potential to bring that same frantic energy to currency markets.

Bias

(80%)

The author expresses concern about the potential for diverging interest rates between the US and other countries, and the impact this could have on global financial markets. She also mentions that Wall Street is benefiting from carry trades as a result of these differentials. While there is no overtly biased language used in the article, there is a clear implication that this divergence could lead to market volatility and potential economic instability.

The thing is, reality has been making a mockery of experts’ assumptions all year long.

This divergence in interest policy, over time, has the potential to bring that same frantic energy to currency markets.

What seems like a slam dunk for Wall Street is not such good news for either the US or the global economy.

U.S. economy has better momentum than other major countries

Real GDP growth estimates have seen significant upward revisions for the U.S.

Household spending, which constitutes roughly 70 percent of GDP, is resilient in the U.S.

Labor market churns out new jobs at a solid pace with higher wages

Inflation has retreated sharply in major developed economies

Headline consumer inflation year over year is between 2 percent and 4 percent for all regions shown

Accuracy

Central bankers are counseling patience regarding a pivot towards less restrictive monetary policy

Global equities have delivered worthwhile gains year to date, with the MSCI All-Country World Index rising roughly 8.5 percent on a total-return basis

Deception

(50%)

The article provides a detailed analysis of the global economic situation and makes predictions about future trends based on current data. However, it does not disclose sources for the statements made within the article. This lack of transparency could lead readers to question the accuracy and reliability of the information presented.

The world economy remains in expansion, though growth trajectories for major countries are uneven.

The United States, as the world’s largest economy, is playing a critical role in global growth amidst weak economic activity in Europe and China.

The International Monetary Fund predicts that the US economy will expand this year at more than twice the rate of other major developed countries.

US consumer-driven economy is supporting growth in the rest of the world.

U.S. and India are generating strong tailwinds for global economic growth, according to Capital Group economists.

The U.S. economy has adapted well to a federal funds rate currently at a 23-year high, ranging from 5.25% to 5.50%.

India’s economy is expected to grow at a rate of 6.8% this year, according to IMF projections, making it a bright star in the emerging markets universe.

Many companies are looking to India as an additional source of manufacturing capacity as China’s economy matures and its real estate market experiences a major downturn.

Elections in various countries, including the U.S., are taking place this year and could result in significant shifts in political leadership, affecting investment environments globally.

A Republican sweep or red wave in the U.S. presidential election could benefit banks, health care companies, and oil and gas companies through deregulation.

A Democratic sweep or blue wave could provide a boost to renewable energy initiatives, industrial stimulus spending and telecommunications projects through additional funding for nationwide broadband access.

Accuracy

Investors and economists expect the Federal Reserve to follow suit and cut interest rates in September.