An increasing number of borrowers are behind on payments for all debt outside student loans

Auto loans saw a $9 billion increase in Q1 2024

Credit card balances decreased but remain near a record high of $1.12 trillion

Credit card delinquencies have risen past pre-pandemic levels with approximately 8.9% of credit card balances transitioning into delinquency in the last year

Household debt reached a new record of $17.69 trillion in Q1 2024

Housing debt balances grew by $206 billion

Mortgage balances rose by $190 billion to $12.44 trillion

In Q1 2024, total household debt reached a new record of $17.69 trillion, an increase of 1.1% from the previous quarter. Mortgage balances rose by $190 billion to $12.44 trillion at the end of March, while credit card balances decreased by $14 billion but remain near a record high of $1.12 trillion.

Household debt balances grew by $184 billion over the previous quarter, slightly less than the moderate growth seen in the fourth quarter of 2023. Housing debt balances grew by $206 billion. Auto loans saw a $9 billion increase, continuing their steady growth since the second quarter of 2020, while balances on other non-housing debts fell in Q1 2024.

Credit card delinquencies have risen past pre-pandemic levels. The percentage of credit card balances in serious delinquency (90 days or more late) reached its highest level since 2012.

According to the New York Fed's Center for Microeconomic Data, an increasing number of borrowers are behind on payments for all debt outside student loans, with delinquency for these debts steadily rising since Q4 2021 after historic lows during the COVID-19 pandemic.

Generation Z borrowers have shorter credit histories and lower credit limits making them more likely to be maxed out on their credit cards and miss a payment. Approximately 8.9% of credit card balances transitioned into delinquency in the last year.

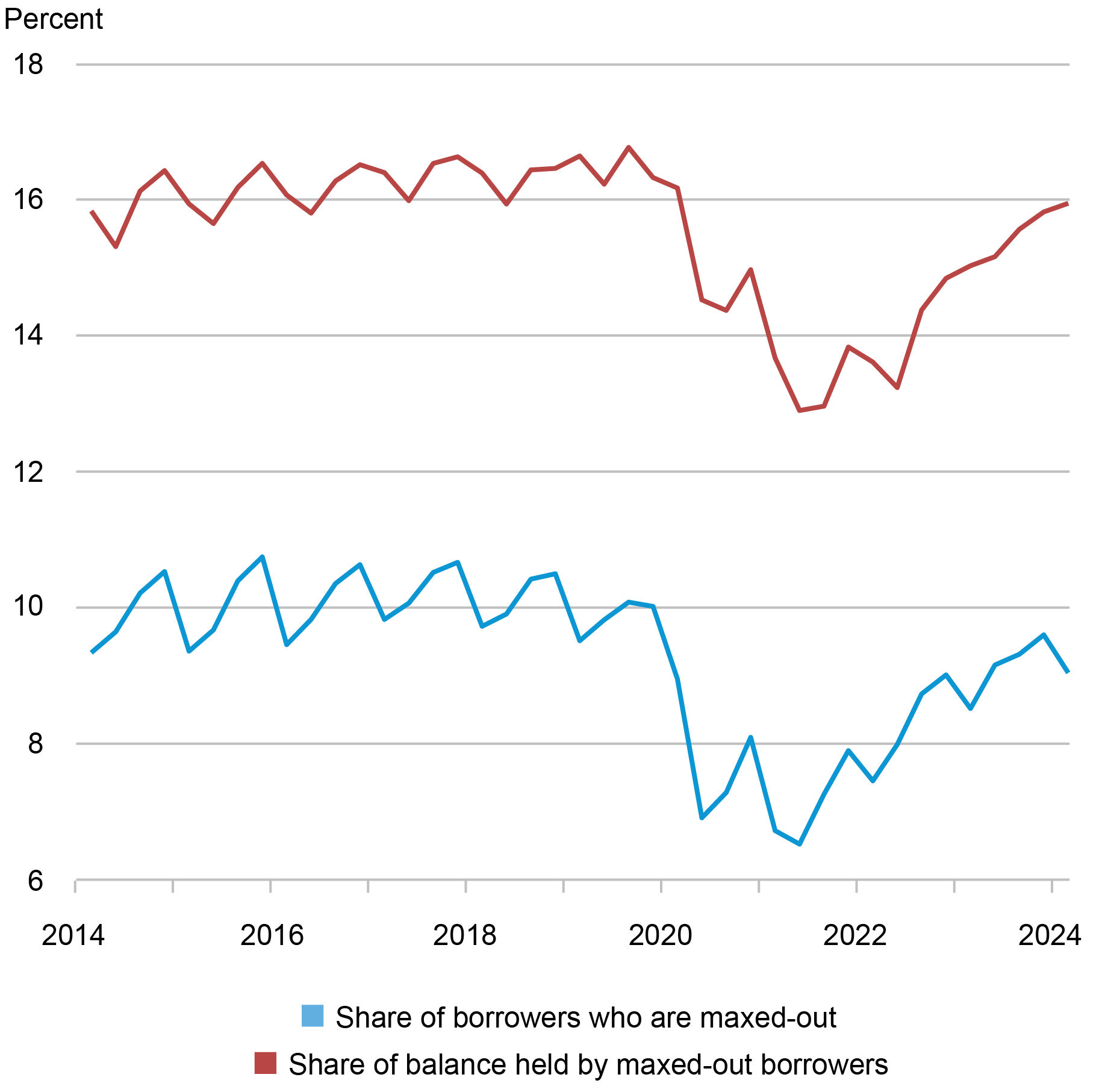

People under 30 and those who live in low-income neighborhoods were particularly likely to be maxed out, with borrowers who make only the minimum monthly payment taking nearly two decades to pay down their debt.

The source of the data on credit card delinquencies is not explicitly stated in the article, it only mentions that it comes from the New York Fed's Center for Microeconomic Data.

Total household debt reached a new record of $17.69 trillion in Q1 2024, an increase of 1.1% from the previous quarter.

Mortgage balances rose by $190 billion to $12.44 trillion at the end of March.

Credit card balances decreased by $14 billion but remain near a record high of $1.12 trillion.

Accuracy

Credit card balances dipped but remain above pre-pandemic levels when adjusted for inflation.

The percentage of credit card balances in serious delinquency (90 days or more late) reached its highest level since 2012.

An increasing number of borrowers missed credit card payments, revealing worsening financial distress among some households.

Deception

(80%)

The article provides factual information about the increase in household debt and delinquency rates. However, there are instances of emotional manipulation and sensationalism that lower the score. The author states 'If people are carrying debt to compensate for steeper prices, they could end up paying more for items in the long run.' This is an attempt to elicit an emotional response from readers by painting a picture of financial hardship and struggle. Additionally, the article uses phrases like 'record amount' and 'astronomically high' to sensationalize the information presented.

The rise in balances comes after the Federal Reserve raised interest rates to a 23-year high

If people are carrying debt to compensate for steeper prices, they could end up paying more for items in the long run.

Fallacies

(90%)

The article reports on the increase in household debt and delinquencies, providing data from the New York Federal Reserve. While there are some instances of inflammatory rhetoric ('astronomically high' interest rates), no formal or informal fallacies were found. However, since there are examples of inflammatory language, the score is reduced to 90.

The rise in debt is particularly concerning because interest rates are astronomically high right now.

People under 30 and those who live in low-income neighborhoods were particularly likely to be maxed out.

Borrowers who make only the minimum monthly payment can take nearly two decades to pay down their debt.

Accuracy

Credit card balances decreased by $14 billion but remain near a record high of $1.12 trillion.

Credit card balances dipped but remain above pre-pandemic levels when adjusted for inflation.

Credit card delinquencies climbed to their highest level since 2012 in Q1 2024.

Deception

(30%)

The article contains selective reporting and emotional manipulation. The author quotes Charlie Wise and Ted Rossman to express concern about the rising credit card delinquencies, but fails to mention that these experts also provide solutions or suggestions for borrowers struggling with debt. This omission creates a sense of hopelessness and despair for readers, who may feel overwhelmed by their financial situation. Additionally, the author uses phrases like 'growing number of borrowers are feeling the strain' and 'pain is not evenly spread' to elicit an emotional response from readers.

People under 30 and those who live in low-income neighborhoods were particularly likely to be maxed out, compared with 4.8% of baby boomers.

About 8.9% of credit card balances fell into delinquency over the last year, a sign that a growing number of borrowers are feeling the strain of rising prices and high interest rates.

Credit card debt is very costly, with the average interest rate topping 20%. Rossman says borrowers who make only the minimum monthly payment can take nearly two decades to pay down their debt.

Fallacies

(85%)

The author uses an appeal to authority fallacy when quoting Charlie Wise and Ted Rossman. He also uses inflammatory rhetoric by stating 'The pain is not evenly spread' and 'That's worrisome, the report says'. However, these statements are not logical fallacies as they are simply reporting on the findings of the reports.

][author] The pain is not evenly spread. That's worrisome, the report says, [[/[

Generation Z borrowers have shorter credit histories and lower credit limits making them more likely to be maxed out on their credit cards and miss a payment

Approximately 8.9% of credit card balances transitioned into delinquency in the last year

Accuracy

Americans owe $1.12 trillion on their credit cards according to a new report from the Federal Reserve Bank of New York

Credit card balances fell by $14 billion in the first quarter of 2024

Credit card delinquency rates rose, especially among young adults aged 18-29

Deception

(30%)

The article makes several statements that are not deceptive on their own but do contain elements of selective reporting and emotional manipulation. The author states that 'credit card delinquency rates rose especially among young adults' without providing any context as to why this is significant or how it compares to previous years. This is an example of selective reporting, as the reader is only given part of the information and not the full picture. Additionally, the author uses phrases like 'high levels of student loan debt' and 'higher prices for food, gas and housing' to elicit an emotional response from readers without providing any concrete evidence or data to support these claims. This is an example of emotional manipulation.

high levels of student loan debt

credit card delinquency rates rose especially among young adults

higher prices for food, gas and housing

Fallacies

(85%)

The article contains several informal fallacies and appeals to authority. It also uses inflammatory rhetoric by highlighting the collective debt amount without context and discussing the challenges faced by Generation Z. The author cites research from the Federal Reserve Bank of New York and Bankrate, which are reputable sources, but does not commit any formal logical fallacies.

. . . credit card delinquency rates rose — especially among young adults, or borrowers between the ages of 18 and 29, who are burdened by high levels of student loan debt and high costs across the board, the New York Fed found.

High inflation and high interest rates are significantly contributing to Americans' debt loads and making this debt harder to pay off.

Not only are their wages lower than their parents' earnings when they were in their 20s and 30s, after adjusting for inflation, but they are also carrying larger student loan balances, recent reports show.

Bias

(95%)

The article does not demonstrate any clear bias towards a specific political, religious, ideological or monetary position. However, the author does use language that depicts young adults (Gen Z) as being more likely to be in credit card debt and miss payments due to their shorter credit histories and lower credit limits. This could be seen as implying that this demographic is less financially responsible than others, which could be considered a subtle form of age bias.

Generation Z borrowers also have shorter credit histories and lower credit limits, making them more likely to be maxed out on their credit cards and miss a payment