Investing during an election year can be challenging but not impossible to navigate successfully.

Maintaining a diversified portfolio and avoiding attempts to time the market based on short-term developments are important strategies for successful investing during an election year.

The 2024 election year is a time of great uncertainty and speculation in the financial markets.

The 2024 election year is a time of great uncertainty and speculation in the financial markets. As campaigns ramp up, promises of policy reform and speculation about their likelihood can have varying impacts on financial markets, leaving many investors questioning the best approach. However, history shows that investing during an election year can be challenging but not impossible to navigate successfully.

One way to stay focused is by maintaining a diversified portfolio and avoiding attempts to time the market based on short-term developments. It's important for investors to focus on long-term economic and business fundamentals, rather than getting caught up in political rhetoric or speculation about policy changes that may not come into fruition.

Investing during an election year can also be a good opportunity to take advantage of market fluctuations. For example, if the stock market experiences a dip early on in the year due to uncertainty surrounding the election results, investors could potentially buy stocks at lower prices and reap rewards as markets recover later in the year.

It's important for investors to stay informed about political developments during an election year but not let them cloud their judgment or lead them away from sound investment strategies. By staying disciplined and focused on long-term economic fundamentals, investors can navigate the challenges of investing during an election year with confidence.

Target Effortless Triple-Digit Gains Every Sunday Evening For Life!

<ul><li>213.3% GAIN on AutoNation calls</li>

Deception

(50%)

The article is deceptive in that it makes false claims about the performance of stocks during election season. The author uses sensationalism and selective reporting to create a misleading narrative.

Target Effortless Triple-Digit Gains Every Sunday Evening For Life!

On Sundays, as a Weekend Plus subscriber, you'll get up to 6 trades every Sunday, each targeting gains of 200% or more.

Fallacies

(100%)

None Found At Time Of

Publication

Bias

(85%)

The article is promoting a product that promises high returns on investment. The author uses language such as 'triple your profit potential' and 'target gains of 200% or more' to create a sense of urgency and excitement for the reader. Additionally, the examples provided are all stock trades with significant gains, which further reinforces this bias.

100.4% GAIN on ON Semiconductor calls

213.3% GAIN on AutoNation calls

On Sundays, as a Weekend Plus subscriber, you'll get up to 6 trades every Sunday, each targeting gains of 200% or more.

Target Effortless Triple-Digit Gains Every Sunday Evening For Life!

Site

Conflicts

Of

Interest (100%)

None Found At Time Of

Publication

Author

Conflicts

Of

Interest (50%)

Patrick Martin has conflicts of interest on the topics of stocks and election season as he is an analyst at Schaeffer's Research. He also has a financial stake in several companies mentioned in the article such as AutoNation, Monster Beverage, Walgreens Boots Alliance, ON Semiconductor, Dell and Apollo Global Management.

Patrick Martin is an analyst at Schaeffer's Research. He has a financial stake in several companies mentioned in the article such as AutoNation, Monster Beverage, Walgreens Boots Alliance, ON Semiconductor, Dell and Apollo Global Management.

The article discusses how stocks tend to perform during election season. Patrick Martin is an analyst at Schaeffer's Research and has a financial stake in several companies mentioned in the article such as AutoNation, Monster Beverage, Walgreens Boots Alliance, ON Semiconductor, Dell and Apollo Global Management.

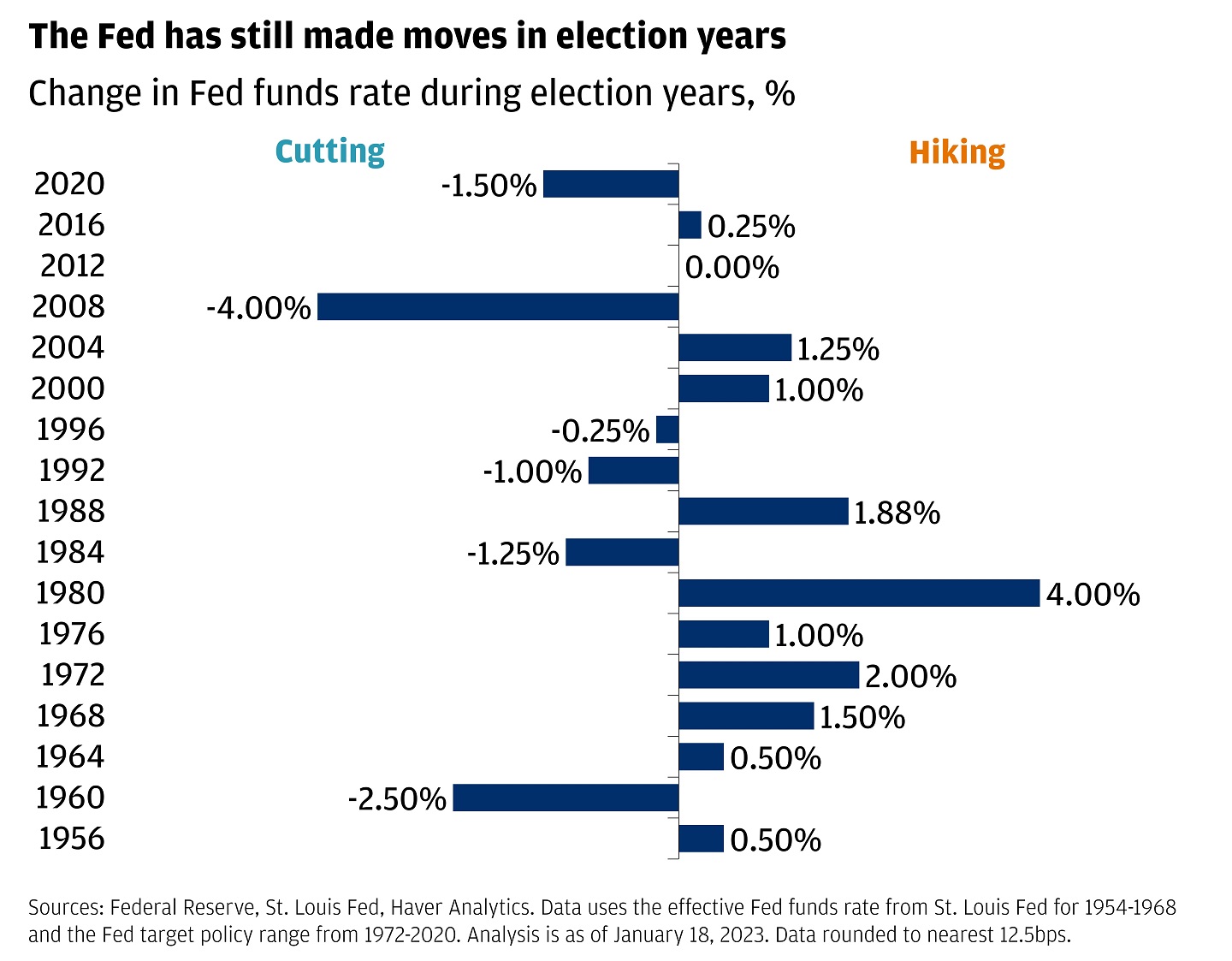

2024 is the year of elections. Over 40% of the world's population and economy will hit the polls to elect national leaders, starting with Taiwan last weekend and culminating with the United States in November.

The upcoming quarterly refunding update from the US Treasury will provide information on how much bond supply there will be

Election debate is only going to ramp up from here. Right now, it's looking like another Biden versus Trump standoff according to prediction markets, favorability polls and most political pundits.

Returns in election and non-election years usually aren't all that different. We took a look at how the S&P 500 has fared in both instances. Going back to 1928 (for as long as we have data), stocks returned an average of 7.5% during election years, compared with 8% during non-election years.

Election years do tend to be more volatile than most, especially in the lead-up to voting day. For instance, the average election year since 1980 has seen an intra-year drawdown of about 17% versus 13% in non-election years.

Accuracy

No Contradictions at Time

Of

Publication

Deception

(30%)

The article is deceptive in several ways. Firstly, the author claims that returns in election and non-election years are usually not all that different. However, this statement is false as shown by the data provided later in the article which shows a slight difference between returns during election and non-election years.

The S&P 500 returned an average of 7.5% during election years compared with 8% during non-election years.

Fallacies

(85%)

The article contains two fallacies: Appeals to Authority and Inflammatory Rhetoric. The author claims that prediction markets, favorability polls and political pundits predict a Biden versus Trump standoff in the upcoming election. This is an appeal to authority as it suggests that these sources are reliable without providing any evidence or reasoning for their predictions. Additionally, the article uses inflammatory rhetoric by stating that

Bias

(85%)

The article contains examples of political bias. The author uses language that depicts one side as extreme or unreasonable by stating 'white supremacists online celebrated the reference to the racist and antisemitic conspiracy.' This is an example of religious bias.

> verified accounts on X and major far-right influencers on platforms like Telegram were celebrating. <

> white supremacists online celebrated the reference to the racist and antisemitic conspiracy. <

"The most promising times for investors for 2024 based on seasonal tendencies alone would seem to be March-August and then November into year-end.'

Accuracy

President Joe Biden

"This year's largest correction very well might happen in February into March on a bounce in rates, along with the period from August into November."

Deception

(30%)

The article is deceptive in several ways. Firstly, the author claims that election years usually have a choppy first quarter in markets but fails to mention that this trend has not been consistent across all election years. Secondly, the author quotes Mark Newton from Fundstrat who states that stocks tend to rise from March to August and then November to year-end during election years without providing any evidence or data for these claims. Thirdly, the article presents a one-sided view of the stock market's performance in 2024 by focusing solely on negative aspects such as tech companies shedding value and rate cut expectations pumping brakes on gains while ignoring positive aspects such as potential post-election relief rally. Lastly, the author uses sensationalism to create a sense of urgency for investors to jump into the market during a potentially choppy start to the year.

The article claims that election years usually have a choppy first quarter in markets but fails to mention that this trend has not been consistent across all election years. For example, in 2016, stocks rose by over 8% from January to March during an election year.

Fallacies

(70%)

The article contains several logical fallacies. The author uses an appeal to authority by citing Mark Newton from Fundstrat as a source for their information. They also use inflammatory rhetoric when they describe the potential largest correction in February into March on a bounce in rates and the period from August into November, which could have negative consequences for investors. Additionally, there is an example of dichotomous depiction when the author describes election years as usually having a choppy first quarter but then stocks tend to rise from March to August and then November to year-end during election years.

The most promising times for investors for 2024 based on seasonal tendencies alone would seem to be March-August and then November into year-end.

Bias

(85%)

The article contains several examples of monetary bias. The author uses language that implies the stock market will experience a correction in February into March and August into November based on past trends without providing any evidence to support this claim.

This year's largest correction very well might happen in February into March on a bounce in rates, along with the period from August into November.

Despite our best intentions, humans make mistakes when investing. We often allow emotions to influence our decisions.

A prudent approach for most investors is to stay the course and show discipline. While elections can introduce uncertainty, focus on long-term economic and business fundamentals, maintain a diversified portfolio, and avoid attempting to time the market based on short-term developments.

Accuracy

A recent survey found 32% of investors believe a recession in the U.S is imminent if the political party with which they least align gains more power in the 2024 federal elections.

Deception

(50%)

The article is deceptive in several ways. Firstly, the author claims that elections have no impact on market returns when history shows otherwise. Secondly, the author uses a survey to make assumptions about investors' beliefs without providing any evidence of their actual behavior or actions based on those beliefs.

The S&P 500’s average return during election years is about the same as non-election years, but it is positive more often. The average return of the S&P 500 in election years was 11.3%, roughly in line with the 11.6% average return in non-election years.

Recessions matter much more to financial markets than political parties.

Fallacies

(85%)

The article contains several examples of informal fallacies. The author uses an appeal to authority by citing a survey conducted by Nationwide and The Harris Poll without providing any evidence or context for the reliability of the source. Additionally, the author commits a false dilemma when stating that investors believe a recession is imminent if their political party with which they least align gains more power in the 2024 federal elections. This statement oversimplifies complex issues and ignores other factors that may influence an investor's decision-making process.

The author cites a survey conducted by Nationwide and The Harris Poll without providing any evidence or context for the reliability of the source.

Bias

(85%)

The author makes a statement that suggests the political party elected in an election year has no impact on market returns. However, this is not supported by historical data as shown in the article's analysis of S&P 500 returns during election years since its creation.

]

Recessions matter much more to financial markets than political parties.

Site

Conflicts

Of

Interest (50%)

Luke Andriuk has a conflict of interest on the topic of investing during an election year as he is affiliated with Saugatuck Financial and serves on their Investment Committee. He also cites data from Nationwide and The Harris Poll in his article.

Author

Conflicts

Of

Interest (50%)

Luke Andriuk has a conflict of interest on the topic of investing during an election year as he is affiliated with Saugatuck Financial and serves on their Investment Committee. He also cites data from Nationwide and The Harris Poll in his article.