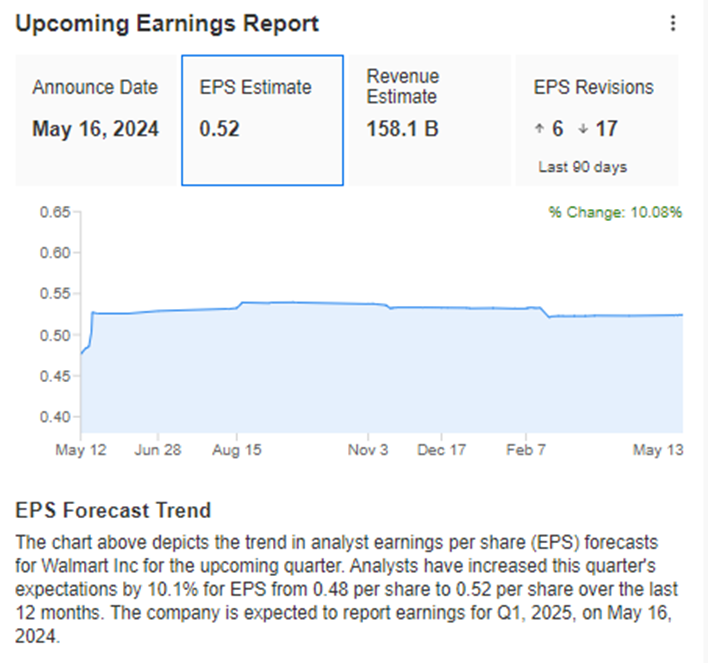

Walmart, the world's largest retailer and a bellwether for consumer spending, is set to report its first quarter earnings on Thursday. The company is expected to release earnings per share of 52 cents on revenue of $159.4 billion, representing an increase year over year of 4.7%. Walmart has been growing in digital advertising, third-party marketplace fees, and fulfillment services, which carry much higher margins than its core retail business.

Approximately 60% of Walmart's annual domestic sales come from groceries. Despite a deceleration in sales growth due to inflationary pressures and an uncertain economy, the company is expected to expand its total gross margin in the quarter to 24.8%. This expansion is driven by these new profit streams.

Walmart has also been investing in other areas, such as opening new outlets and modernizing existing stores. The company plans to open 150 new outlets and modernize 1,400 stores over the next five years. It recently announced a $2.3 billion acquisition of smart TV maker Vizio to expand its advertising opportunities in the electronic sales market.

Consumer spending resilience has been indicated by recent earnings reports from travel-related companies, but some analysts have warned of cracks emerging among lower-income shoppers. Walmart's strategy of targeting more affluent consumers by prominently displaying higher-quality, higher-priced items and launching its premium grocery brand, Bettergoods, may help the company weather any potential consumer pullback.

The retail earnings season is underway and will shed more light on the health of American consumers and the strength of the industry. Investors will be closely watching Walmart's financial forecast for guidance on the quarter and year ahead.